It isn’t uncommon for businesses to experience property loss. Whether small or large, loss will most likely happen at some point in the lifetime of a business. Most businesses have some type of property that is used in the operation of the business. But how do you determine the type of business property and its value? And what is the difference between actual cash value versus replacement cost when it comes to property loss reimbursement?

Every business needs various forms of insurance – even the smallest home-based businesses need coverage. It’s important to note, your homeowner’s policy isn’t designed to cover activities that involve a small business. Having coverage for an unexpected loss could mean the difference between getting back to business or being forced to close permanently.

So, what is considered commercial property?

Commercial property falls into two categories. They will either be classified as real property or business personal property.

Examples of real property include the land, buildings, and equipment or machinery that is a permanent fixture. They typically are not removed from the business’s premises.

Business personal property is equipment or materials that can easily be moved from one location to another, such as furnishings or electronics.

Understanding Actual Cash Value versus Replacement Cost

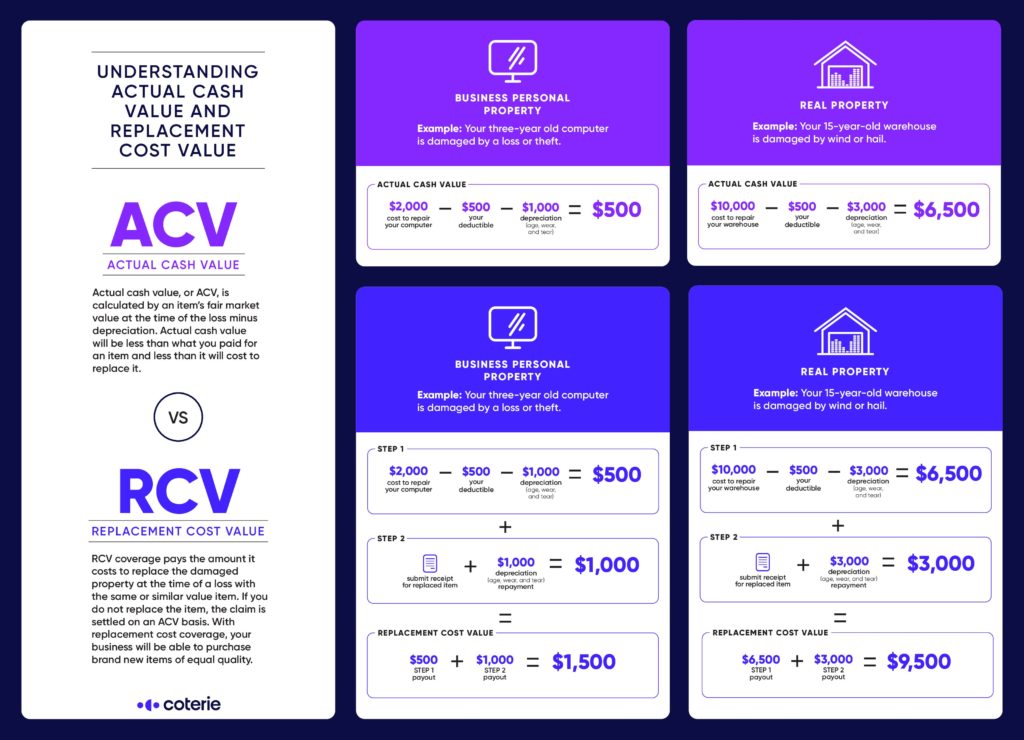

Actual cash value, or ACV, is calculated by an item’s fair market value at the time of the loss minus depreciation. Actual cash value will be less than what you paid for an item and less than it will cost to replace it. ACV policies tend to be less expensive than replacement cost policies.

Replacement cost coverage pays the amount it costs to replace the damaged property at the time of a loss with the same or similar value item. With replacement cost coverage your business will be able to purchase brand new items of equal quality.

In the event of a loss, some insurance companies won’t give you money before you replace your damaged or stolen property. The business will likely need to repurchase the property first and depending on the type of coverage the insurance company will reimburse either actual cash value or replacement cost. Understanding the difference in coverage is an important consideration. Know what type of coverage you are purchasing before you have a claim.

How can you know which reimbursement applies to you and your business, though?

Here are some examples:

- With respect to Business Personal Property, your three-year old computer is damaged by a loss or theft. The fair market value of that computer would be determined based on what it’s worth at the time of loss, then depreciation would be subtracted based on the age and wear and tear of the computer. Your policy will compensate you for the value of a three-year-old computer. This is actual cash value.

- With respect to a Building, your 15-year-old warehouse is damaged by wind or hail. A repair estimate will be written, and we apply depreciation to materials such as a roof or siding based on age. Your policy will compensate you for the repairs less applicable depreciation. This is actual cash value.

- For replacement cost, the same three-year-old computer can be replaced with a brand-new computer of a similar make, model, and quality. The initial claim payment would be at Actual Cash Value. Once you replace the item brand-new and submit your replacement receipt, you will be reimbursed any depreciation that was withheld from the initial claim payment.

- With respect to a Building, your 15-year-old warehouse is damaged by wind or hail. A repair estimate will be written, and we apply depreciation to materials such as a roof or siding based on age. The initial claim payment would be Actual Cash Value. Once all building repairs are completed, you can submit your final repair invoice and become eligible for reimbursement of any depreciation that was withheld from the initial claim payment. This scenario represents replacement cost.

Have questions about insurance coverage for your business? Head to our Find An Agent page to connect with a licensed insurance expert in your area.